File 4: Israel’s corporate giants at home in the Netherlands

SOMO’s ‘The Netherlands-Israel Investment Files’ series explores how the Netherlands became Israel’s investment clearing house.

Key insights

- Two of Israel’s largest corporations have set up their regional European head office in the Netherlands. These Israeli corporate giants use Dutch companies to pump billions into their global operations.

- Israeli chemicals company ICL has its European headquarters in the Netherlands. ICL chose the Netherlands as its regional headquarters in 2014 after extensive lobbying by the Dutch government and the offer of favourable tax treatment. The State of Israel has a “Special State Share” in ICL to “safeguard” its vital interests.

- Israel’s largest private employer and one of the world’s largest generic drug manufacturers, Teva Pharmaceuticals, has its European headquarters in the Netherlands. It has set up a web of financing and holding companies in the Netherlands and uses Dutch companies to channel billions in financing to group companies.

Two of Israel’s largest corporations have set up their regional European head office in the Netherlands: Teva Pharmaceuticals, Israel’s largest private employer, and chemicals giant Israel Chemicals Limited (ICL Group). These Israeli corporate giants use Dutch companies to pump billions into their global operations.

Israel Chemicals Limited (ICL)

Israeli chemicals company ICL has its European headquarters in the Netherlands. ICL chose the Netherlands as its regional headquarters in 2014 after extensive lobbying by the Dutch government and the offer of favourable tax treatment. The State of Israel has a “Special State Share” in ICL to “safeguard” its vital interests.

Israel Chemicals Limited, now known under the abbreviation ICL produces fertilisers and other chemicals and is one of Israel’s largest companies. Its 2024 revenues amounted to $7 billion(opens in new window) . The controlling shareholder of ICL is the Israel Corporation(opens in new window) , one of Israel’s largest conglomerates, which holds 44 per cent of the shares. ICL was government-owned until its privatisation and takeover(opens in new window) by the Israel Corporation in the 1990s. However, the State of Israel still has a “Special State Share”. This gives it the “right to safeguard the State of Israel’s vital interests” , which it can do, for example, by blocking a shareholder from acquiring shares or control of the company.

ICL has been active in the Netherlands since 1976, when it acquired a bromine processing factory in Terneuzen(opens in new window) , after which it acquired a fertiliser factory in Amsterdam(opens in new window) in 1982. Its Amsterdam factory has received complaints from surrounding residents of smoke and “a heavy chemical air that hits you in your face”(opens in new window) , causing physical impacts such as burning eyes, sore throat and stress. In 2015, ICL opened(opens in new window) its European head office in the Netherlands.

ICL struck a tax deal with the Dutch tax authority

According to reporting by the Dutch newspaper NRC(opens in new window) on the basis of Freedom of Information requests, ICL’s decision to base its European head office in the Netherlands in 2015 was the result of an extensive lobbying process(opens in new window) by then Prime Minister Mark Rutte and the Ministry of Economic Affairs.

ICL’s CEO reportedly(opens in new window) only wanted to move to the Netherlands if the company would receive tax treatment similar to that it would obtain in Switzerland, which it was also considering as a location. In Switzerland, ICL would have to pay an effective tax rate of just 10 per cent. After ICL’s CEO had a meeting with a senior official of the Ministry of Economic Affairs in February 2014, the Netherlands Foreign Investment Agency (NFIA), an institution of the Ministry of Economic Affairs, sent him a letter advising him to start talks with the Dutch Tax Authority, which would show him “how favorable a ruling would be in your case”. The NFIA even offered to pay(opens in new window) for up to half of consultancy firm KPMG’s fiscal advice to ICL, up to a maximum of €25,000.

In 2014, the Dutch Tax Authority’s tax ruling offered ICL an effective tax rate that, according to the Ministry of Economic Affairs, “met the expectations of ICL”(opens in new window) . It is beyond the scope of SOMO’s current analysis to determine how this result was achieved and whether the tax ruling is still in force, but the extent to which the Dutch authorities appeared willing to go to seduce ICL’s investment is notable.

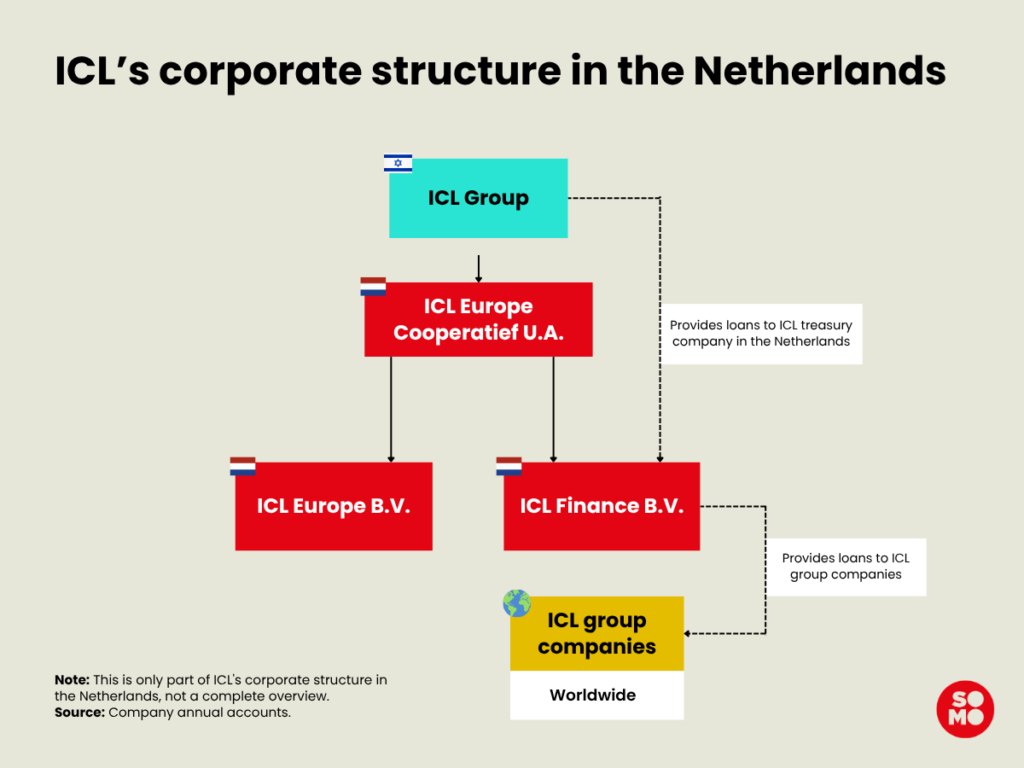

Corporate structure of ICL in the Netherlands

ICL has two Dutch companies, ICL Europe Cooperatief UA and ICL Europe B.V., that act as its purchasing and sales organisations in Europe. ICL Europe Cooperatief has €3 billion in assets and recorded a revenue of €1.2 billion in 2023.

Since 2004, ICL has also used a Dutch company to provide financial services to group companies. This company, ICL Finance B.V., has no employees but large financial assets, and can therefore be referred to as a letterbox company. ICL Finance B.V. provides and receives loans to and from group companies. It has over €3 billion in assets. In 2024, the company provided €1.9 billion in long-term loans and €1 billion in short-term loans to group companies. It received €1.5 billion in loans from group companies, including from its Israeli parent company . CL Finance B.V. received €143 million in interest income from group companies in 2024. It also made €123 million in interest payments to group companies in the same year.

The Netherlands is frequently used by multinational corporations as a conduit country(opens in new window) for loan financing, due to the general absence(opens in new window) of withholding taxes on interest payments. POP-UP: Governments levy withholding taxes on companies paying out interest, dividends, and royalties. The Netherlands has one of the highest numbers of tax treaties(opens in new window) globally, which generally reduce such withholding taxes. This makes the Netherlands an attractive conduit country for this type of financial flow. The Netherlands only levies a withholding tax on outgoing interest, royalty and dividend payments to companies in jurisdictions that are listed as “non-cooperative jurisdictions”(opens in new window) by the EU and/or have a profit tax below 9 per cent, which includes Bermuda and The Bahamas. This is the “conditional withholding tax”, introduced in 2021, which SOMO has criticised as flawed because it only applies to a very select few countries.

Ownership of ICL

The Netherlands also plays a role in the overall ownership of ICL. As noted above, the controlling shareholder of ICL is the Israel Corporation(opens in new window) with 44 per cent of the shares. Israel Corporation is Israel’s largest holding company and owned(opens in new window) by Israeli billionaire Idan Ofer. Idan Ofer holds his shares in Israel Corporation through a number of corporate entities. One of these is Ansonia Holdings Singapore B.V., a company registered in the Netherlands with a branch in Singapore.

While the effective management of Ansonia Holdings Singapore B.V. is located in Singapore, the company is registered in the Netherlands, submits its annual reports to the Dutch Chamber of Commerce and is audited by a Dutch independent auditor. According to its 2023 annual accounts, this company has $2.3 billion in assets.

Teva Pharmaceuticals

Teva Pharmaceuticals, one of the world’s largest generic drug manufacturers, has its European headquarters in the Netherlands. It has set up a web of financing and holding companies in the Netherlands and uses Dutch companies to channel billions in financing to group companies.

Teva Pharmaceuticals is one of the world’s largest generic drug manufacturers. The company recorded revenue(opens in new window) of $16.5 billion in 2024 and holds 10 per cent(opens in new window) of the global market share in generic medicine.

Teva has been a supporter of the Israeli military for many years, including during the genocide in Gaza. In a 2024 interview(opens in new window) that focused on what he termed “the war”, Teva’s CEO said that he tries to “give a perspective and a voice of Israel, which can be somehow drowned out because of how the media operates”.In 2016, Teva supported(opens in new window) the Israeli military through the “Adopt a Battallion” programme. A number of Danish pension funds divested(opens in new window) from Teva in 2025 over concerns regarding the company’s ties to the Israeli military.

Teva’s web of Dutch companies

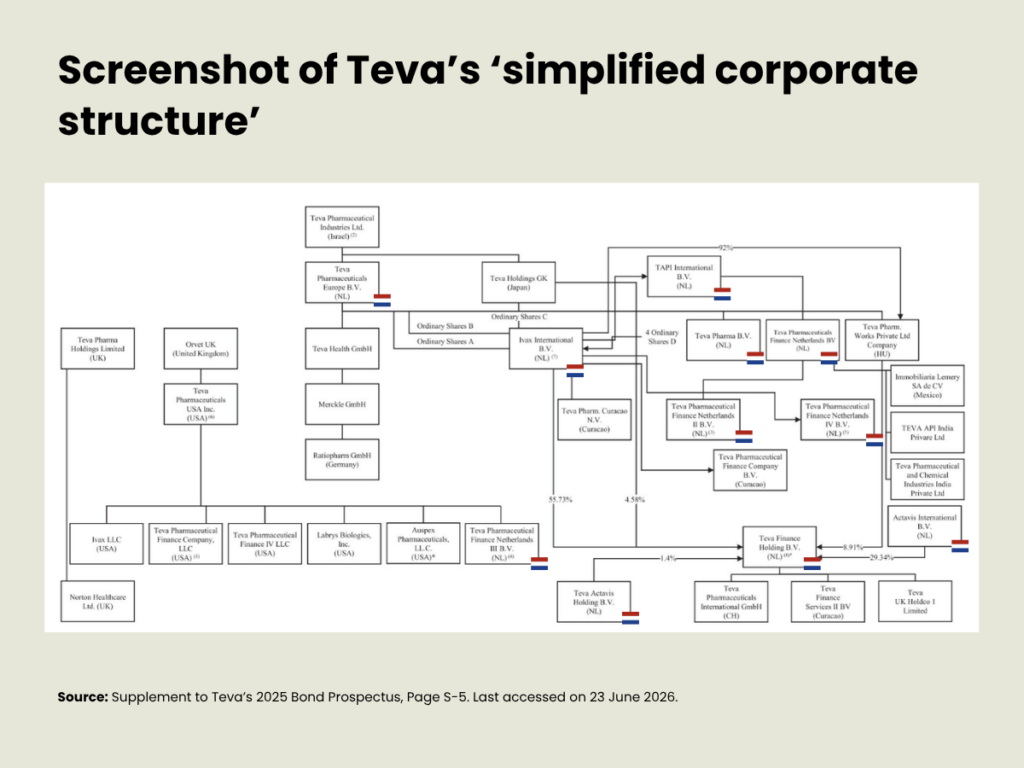

Teva has its European head office in the Netherlands and uses the country as its global financial hub, operating a web of financing and holding companies that hold billions in assets. The screenshot above shows Teva’s “simplified corporate structure” as included in a 2025 bond prospectus(opens in new window) . The Dutch flags mark the Dutch companies and are added by SOMO.

Teva uses a Dutch company, Teva Pharmaceuticals Europe B.V., as its European headquarters and holding company. This company owns Teva’s subsidiaries in the US, Germany, and the UK, among others. It holds €11.7 billion in financial assets and recorded revenue of €225 million in 2022, based on its last available annual accounts.

Teva also uses a number of Dutch letterbox companies to issue billion-dollar bonds and provide financing to group companies. SOMO examined this structure.

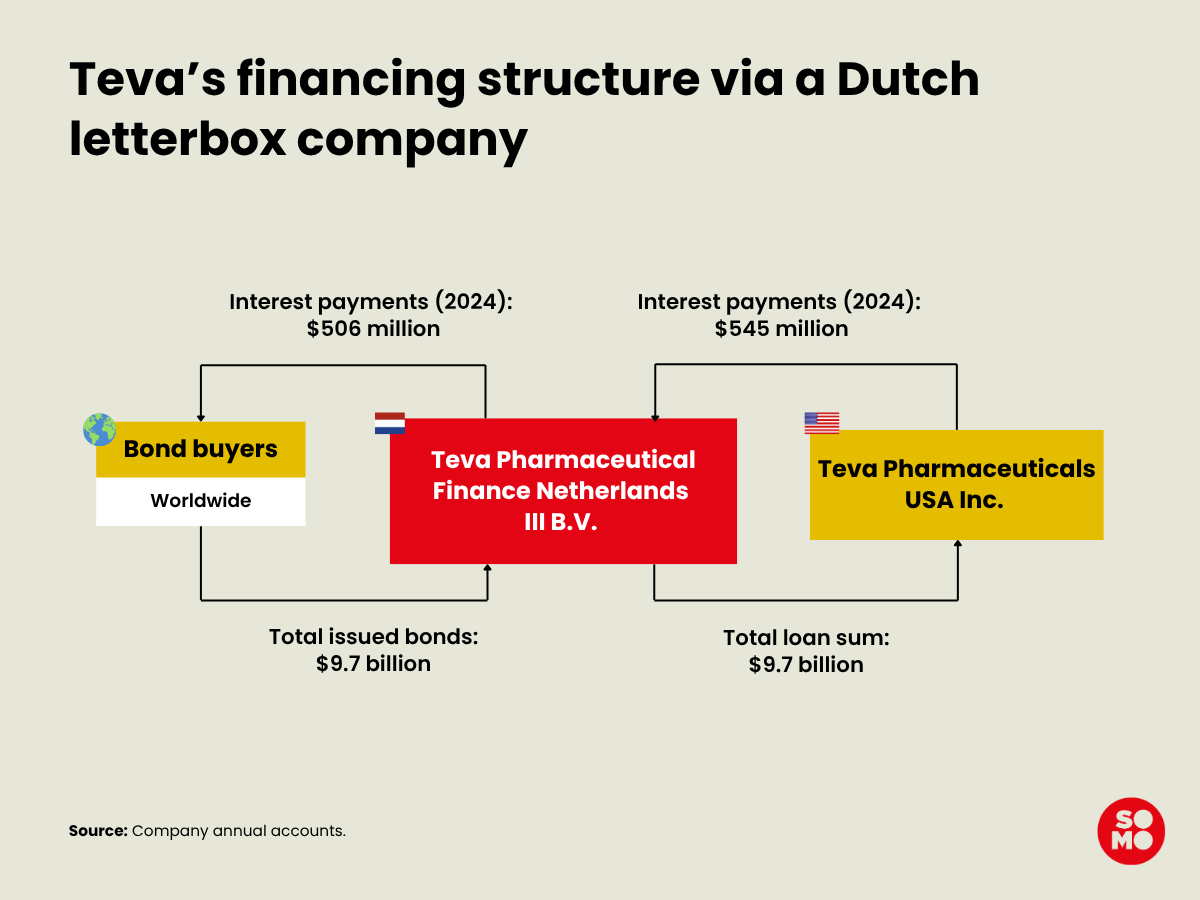

Dutch letterbox companies used as a conduit

Teva has three companies in the Netherlands with a similar purpose: raising funds by issuing bonds, and loaning the proceeds of these bonds onto group companies. Each company issues bonds in a different currency: Teva Pharmaceutical Finance Netherlands II B.V. (euros); Teva Pharmaceutical Finance Netherlands III B.V. (US dollars); and Teva Pharmaceutical Finance Netherlands IV B.V. (Swiss francs). These companies have no employees and sizable financial assets, which is why they are referred to here as letterbox companies.

According to its 2024 annual report, the purpose of Teva Pharmaceutical Finance Netherlands III B.V. is to “support the current financing requirements of Teva Pharmaceutical Industries Limited”, Teva’s Israeli parent company. It describes its activities as follows: the company “obtains funds from the market by issuing corporate bonds/notes” and the “net proceeds of these notes are lent on in the form of related party loans to Teva Pharmaceuticals USA Inc.” The Dutch letterbox company acts as a conduit between the buyers of Teva’s bonds and Teva’s US subsidiary.

As of 2024, Teva Pharmaceutical Finance Netherlands III B.V. has eight outstanding bonds issued between 2016 and 2025, totalling $9.7 billion. The proceeds from all these bonds are entirely lent to Teva’s US subsidiary. Teva Pharmaceutical Finance Netherlands III B.V. received $545 million in interest income in 2024 from the loans it issued to the US entity, while spending $506 million on interest payments on its outstanding bonds.

The Netherlands only levies a withholding tax on outgoing interest payments to companies in jurisdictions that are listed as “non-cooperative jurisdictions”(opens in new window) by the EU and/or have a profit tax below 9 per cent, such as Bermuda and The Bahamas. This is the “conditional withholding tax”, introduced in 2021, which SOMO has criticised as flawed because it only applies to a very select few countries. If the bond holder is not in one of the countries designated by the Netherlands as a low-tax jurisdiction, no tax is withheld on interest payments.

The US and the Netherlands have a tax treaty which includes a 0 per cent(opens in new window) withholding tax rate on interest payments. This means that there is also no withholding tax charged on the interest payments made by the US subsidiary to the Dutch letterbox company. The US-Israel tax treaty includes a 17.5 per cent (opens in new window) withholding tax rate on interest. Teva’s use of a Dutch letterbox company to issue bonds and loans raises questions about possible tax avoidance.

Do you need more information?

-

Jasper van Teeffelen

Researcher

More from this series

-

File 1: Flag swapping capital: a Dutch investment servicePosted in category:News

File 1: Flag swapping capital: a Dutch investment servicePosted in category:News Jasper van TeeffelenPublished on:

Jasper van TeeffelenPublished on: -

File 2: Indefensible: Dutch support to Israeli arms manufacturersPosted in category:News

Jasper van TeeffelenPublished on:

File 2: Indefensible: Dutch support to Israeli arms manufacturersPosted in category:News

Jasper van TeeffelenPublished on: -

File 3: Double-edged digital: Netherlands as Israel’s tech portPosted in category:News

Jasper van TeeffelenPublished on:

File 3: Double-edged digital: Netherlands as Israel’s tech portPosted in category:News

Jasper van TeeffelenPublished on: -