The real winners of the AI Race

Microsoft, Amazon, Google and Nvidia

The so-called “AI Race” is dominating business and policy discussions on technology. With companies and states competing to conquer the developing genAI market, start-ups like OpenAI(opens in new window) , Anthropic, and Mistral(opens in new window) are often viewed as national champions with the potential to challenge the dominance of Big Tech. However, SOMO’s analysis of the value chains of the 12 most valuable genAI start-ups tells another story: start-ups are highly dependent on Big Tech firms.

Key findings:

- Start-ups are highly dependent on Big Tech firms:

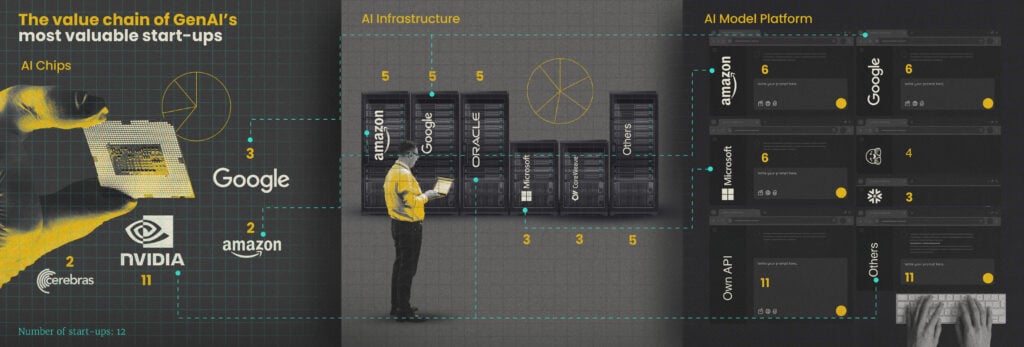

- 11 start-ups use Nvidia for the AI-specialised chips used to train and deploy genAI;

- 10 rely on Amazon, Microsoft, and Google for the AI infrastructure needed to train and run their models; and

- 9 commercialise their models via Amazon, Microsoft, and Google platforms.

- Big Tech companies have also established partnerships with genAI start-ups, increasing their ability to dominate the development and commercialisation of AI.

- GenAI start-ups do little to fostering diversity or competition in digital markets. Big Tech companies continue to exercise significant control over the market for new products, even those developed by other companies.

- As AI is increasingly taken up by business and public services, public authorities – particularly competition regulators – must scrutinise the market closely and act decisively to prevent greater concentration of power.

The complex value chain of genAI

Generative AI (genAI) is a type of artificial intelligence system that can create new outputs, including text, images, code, audio, and video, with OpenAI’s ChatGPT being the most well-known. These systems are built upon a complex value chain(opens in new window) , in which each link continuously interacts with the other.

SOMO analysed the value chains of 12 genAI start-ups, mapping key components of each company’s operations, including chips, infrastructure, data sources, data workers, and capital. (Read more about our methodology here.)

In this article, we explore the hardware, infrastructure, and platform components of the value chain of the most valuable start-ups developing genAI models. While there is a diversity of models, our analysis reveals that genAI start-ups rely on Big Tech firms for key inputs and paths to market. The market power of Big Tech companies means that new players, even significant innovators in AI, are highly dependent on them.

Nvidia dominates the design and sale of AI chips

At the core of GenAI’s value chain are specialised AI chips. Such chips are optimised for the heavy workload of processing data in order to find patterns (training AI models) and providing results to users’ queries (inference).

In our sample, 11 of the 12 start-ups used Nvidia AI chips, such as A100 or H100 Graphic Processing Units (GPUs). In fact, Nvidia dominates the AI chip design market, with a market share(opens in new window) ranging from 80% to 95%. The company’s pre-eminence is not due solely to its chip design, but also to the software used to optimise its chips, Compute Unified Device Architecture (CUDA). CUDA has been described as Nvidia’s “moat”(opens in new window) , the technical advantage that isolates it from competition.

Some start-ups also used chips from Amazon, Google, Microsoft, and Cerebras. However, these seem to be complementary to Nvidia’s products, rather than replacements.

Overall, the genAI explosion has been a boon for Nvidia, which, as of June 2025, was valued(opens in new window) at 3.44 trillion dollars, a 753% increase in value since the launch of ChatGPT, which was developed on a large number of Nvidia chips. The company has also substantially increased its profitability with an operating margin(opens in new window) of 55.5% in 2024.

Nvidia’s dominance in the AI chip market has raised competition concerns. Most prominently, the company has been under investigation(opens in new window) by the French competition authority for anti-competitive practices. While no charges have been made at the time of writing, the competition authority has stated(opens in new window) that Nvidia’s dominance could allow it to fix prices, limit production, impose unfair conditions, and discriminate between clients.

Amazon, Google, and Microsoft own the AI infrastructure

GenAI companies not only need highly advanced AI chips, they need a lot of them. The training and inference phases of genAI development can require significant computing power, depending on the complexity of the model and the size of the dataset. To train Luminous Supreme, for instance, Aleph Alpha used a cluster of 512(opens in new window) Nvidia A100 GPUs, while OpenAI GPT-3 was reportedly(opens in new window) trained on 10,000 Nvidia A100 GPUs.

AI start-ups have three options(opens in new window) for getting access to the volume of chips they need. First, they can buy the chips directly and build their own clusters. Second, they can use a public supercomputer. Or third, they can buy access to clusters housed in a cloud provider’s data centres.

Most of the start-ups SOMO analysed have chosen to buy access via a cloud provider, with Amazon, Oracle, Google, and Microsoft being the most frequently used. Amazon, Google, and Microsoft especially have an immense advantage in the cloud provider market. For years, they have been building up a wide network of data centres, including AI-specialised ones, to support their growing cloud businesses. As Microsoft put it in its 2023 report:

“Four years ago, we first invested in our AI supercomputer, with a goal of building the best cloud for training and inference. Today, it’s being used by our partner OpenAI to power its best-in-class foundation models and services, including one of the fastest-growing consumer apps ever—ChatGPT. Nvidia, as well as leading AI start-ups like Adept and Inflection, is also using our infrastructure to build its own breakthrough models.”

From 2015 to 2024, Amazon, Google, and Microsoft spent a combined €671.96 billion on land, buildings, and equipment, with a noticeable increase in spending since 2020. According to the companies’ annual reports, this spending increase has mostly been driven by the procurement of AI chips and the expansion of AI data centres.

Amazon, Google, and Microsoft are so dominant that they are not threatened by new AI Cloud providers. According to the UK’s competition authority(opens in new window) , AI-specialised providers, like CoreWeave, have much smaller capacity, so their entry into the market has not affected the position of the bigger players.

On top of their capacity advantage, the three cloud providers have actively pursued business with genAI start-ups, providing discounted rates for multi-year contracts or offering commercial partnerships in which the genAI model-maker is given access to the cloud infrastructure in exchange for preferential access to the model itself. For example, Microsoft provided OpenAI with AI infrastructure in exchange for the exclusive right to sell access to GPT models via its Azure cloud. The original partnership agreement forbade OpenAI from seeking complementary cloud infrastructure elsewhere. Although this provision has since been renegotiated(opens in new window) , Microsoft retains the right of first refusal, meaning OpenAI can only use another provider if Microsoft refuses to provide the requested service.

Microsoft’s investment in Mistral, a French start-up, also required(opens in new window) a commitment to use its cloud infrastructure and the possibility to collaborate on “training industry-specific models for selected customers and support for European public sector workloads.”

Using Big Tech’s infrastructure is by far the most common choice for genAI start-ups, yet, three start-ups have tried alternative models:

- For xAI, Elon Musk leveraged(opens in new window) his ownership of X (formerly Twitter) and Tesla to get access to Nvidia chips, while also complementing the chips with cloud services from Amazon and Oracle. Later, xAI built a mega-data centre in Memphis(opens in new window) (US).

- Aleph Alpha built its own modest data centre, then expanded its processing power by using cloud services from Oracle, Stackit, and Hewlett-Packard Enterprise (HPE)(opens in new window) .

- Hugging Face’s model, Bloom, was trained(opens in new window) on a public infrastructure, the Jean Zay Public Supercomputer, which was provided and subsidised by the French government. This is the only genAI model in the SOMO sample(opens in new window) that used public infrastructure. However, Hugging Face’s StarCoder model was trained on Amazon’s infrastructure.

These examples show alternatives like building your own infrastructure or using public infrastructure are possible, but are limited to either smaller projects or start-ups owned by the world’s richest man.

The environmental footprint of genAI’s data centres

Analysing the role of data centres in the genAI value chain is important for understanding the market power advantages of Big Tech, as well as the environmental implications of genAI technology. The AI boom has led to an explosion of data centres, which have high energy and water consumption. According to the International Energy Agency(opens in new window) , “a typical AI-focused data centre consumes as much electricity as 100,000 households, but the largest ones under construction today will consume 20 times as much.”

The non-profit organisation, Beyond Fossil Fuels, has warned that new data centres in Europe may threaten(opens in new window) the energy transition, either by increasing the consumption of fossil fuels or by consuming the renewable energy needed to decarbonise other sectors. Recently published research shows that AI companies generally do not disclose(opens in new window) the environmental impacts and resource consumption associated with their products. In fact, transparency on these issues has decreased since the launch of ChatGPT.

Amazon, Google, and Microsoft increasingly dominate the pathway to market

Most genAI start-ups are still struggling to find a profitable business plan that offsets the extremely high costs of production and deployment. One possibility is selling direct access to their genAI models, allowing businesses, developers, and public bodies to use the base model and fine-tune it to their particular needs. All but one of the start-ups SOMO analysed were pursuing this approach.

However, Big Tech companies have quickly leveraged their dominance in the cloud to become the platform for connecting genAI start-ups with private and public customers. Amazon Bedrock, Amazon SageMaker, Microsoft Azure, and Google Vertex are providing their cloud customers with access to genAI models developed by themselves and others, as well as a variety of tools for fine-tuning and deploying genAI.

Of the 12 start-ups analysed, nine have allowed their models to be hosted on Big Tech platforms. Amazon, Google, and Microsoft dominate(opens in new window) the global cloud market, making them an important gateway to consumers.

This is perfectly illustrated by the European Parliament’s decision to use Anthropic’s Claude model to run its historical archives. Research by the Irish Council for Civil Liberties (ICCL)(opens in new window) revealed that the Parliament’s choice of model was limited to models available on Amazon Web Services. This was because the EU Institutions are bound by a cloud procurement agreement(opens in new window) with Amazon. As ICCL put(opens in new window) it: “The Parliament is locked into Amazon’s Cloud ecosystem and relies on Amazon Bedrock –Amazon’s marketplace for AI models.”

As with the provision of AI infrastructure, Big Tech companies did not merely rely on their existing market advantages to attract the genAI model-makers. They used commercial partnerships, offering discounted and privileged access to cloud services or financial investments, in exchange for the right to commercialise the model. Some agreements even include exclusivity provisions, such as OpenAI’s agreement with Microsoft. Amazon’s partnership with Anthropic includes an agreement to provide Amazon clients with early access(opens in new window) to the start-up’s models. In response to SOMO’s queries, an Anthropic spokesperson stated that Amazon’s $ 8 billion investment(opens in new window) in the start-up and the early access for Amazon customers were agreed separately.

Only three genAI model-makers are not available via Big Tech clouds:

- Inflection AI(opens in new window) and Adept AI(opens in new window) were recently the subject of takeovers, commonly called acqui-hires, by Microsoft and Amazon, respectively, who poached most of the genAI start-ups’ employees and bought their intellectual property directly.

- The German Aleph Alpha has mostly shunned any relationship with Big Tech, except for Nvidia.

Data workers

Value chains dominated by a few corporate players often enable the exploitation of smaller suppliers and workers. In genAI, workers who label and clean data, and test the models are crucial. However, there is mounting evidence of exploitation of these workers, who are often hired via third parties such as outsourcing companies and crowdwork platforms. Data workers, especially those in Global South countries, have reported(opens in new window) poor working conditions, with little to no protections and low pay.

Even here, Big Tech’s footprint can be seen. Amazon pioneered crowdwork when it launched(opens in new window) the Mechanical Turk platform in 2005. Almost 20 years later, Meta announced a deal to buy 49% of the controversial AI crowdwork platform, Scale AI.

AI’s platform moment

The importance of model hosting for Big Tech can be seen by the fact that Microsoft rushed(opens in new window) to host Deepseek’s family of genAI models even though they directly challenged the primacy of Microsoft’s partner, OpenAI. More recently, Microsoft announced it would host xAI’s models, even though its owner, Elon Musk, is currently suing Microsoft and OpenAI.

For Amazon, Google, and Microsoft, hosting these models is a way to reinforce(opens in new window) their cloud businesses. Aleph Alpha’s CEO made this point(opens in new window) very clearly when the start-up decided to stop pursuing large models:

“It’s hard to make it make sense economically. It’s not hard to wire a lot of money to Nvidia. Everybody can do that. But it’s hard to build a working business model…. There are strategic interests that are disrupting this market. Tech giants aren’t seeing this as a working business model by itself, but as a tool to strengthen existing models. They don’t need to get an ROI [Return on Investment] on [this] investment.”

Microsoft’s CEO, Satya Nadella, has articulated a different view, recently proclaiming(opens in new window) this moment to be “another platform shift”. Previous platform(opens in new window) shifts saw Big Tech companies become gatekeepers for key parts of the digital economy, from online marketplaces to app stores to social media. This allowed them to impose exploitative conditions on users and extract immense data and financial fees. The role of Big Tech in the genAI market development is likely to follow a similar pattern.

Big Tech companies’ dominance in cloud services has been studied by several competition authorities across the world. According to a recent investigation by the UK competition authority(opens in new window) , Big Tech firms see the provision of access to AI models as a way to attract customers to their cloud and get them to buy adjacent services. Internal documents seen by the authority show that Amazon, Google, and Microsoft have all experienced rapid growth in the use of and revenue from their AI platforms and broader cloud offerings.

The French Competition Authority(opens in new window) has highlighted how Amazon, Google, and Microsoft used a range of practices to lock in customers, from providing free cloud credits to making it very expensive and technically difficult to leave their cloud. The UK competition authority pointed out that the same practices will affect the AI market, while the French authority says such practices are already intensifying(opens in new window) . This means that AI customers are likely to find it hard to switch or even use multiple cloud providers at once, locking them into Big Tech’s services.

State support to AI ‘national champions’ may backfire

In the past year, states have entered the “AI race” to protect and support companies they deem national AI champions. The United States(opens in new window) , France(opens in new window) , and Canada(opens in new window) have all announced public support for private investments in AI data centres.

Direct support has been accompanied by deregulation efforts. In the US, legislators sought(opens in new window) to impose a 10-year ban on state-level AI regulation, while in France, the government wants to enable(opens in new window) the development of very large data centres, overriding local administrations, speeding up consultation with local communities, and enabling derogation from environmental rules.

Yet the start-ups these initiatives claim to support (OpenAI, Mistral, and Cohere) are deeply enmeshed with Big Tech. Some of the projects that end up being supported might even directly benefit Big Tech, such as France’s support for the AI data centre being built(opens in new window) by the Microsoft-backed company G42.(opens in new window)

Without breaking the dependency and deep interlinkages between AI start-ups and Big Tech, public interventions in the “AI race” are likely to further entrench the power of the dominant tech companies. This will, in turn, exacerbate the environmental and social harm built into the Big Tech model.

The role of competition tools

Competition authorities from the UK, France, Portugal, the US, and others have found signs of anti-competitive practices in genAI markets. A lot of attention has been paid to partnerships between Big Tech and AI start-ups and whether they qualify as mergers. Some have gone deeper, analysing how Big Tech’s market power and position have enabled it to dominate developing AI markets. A list of competition authorities’ work on genAI is available here. Despite expressions of concern by competition authorities, none have intervened to address the role of Big Tech in the evolution of the AI market.

There is a grave risk that Big Tech will end up dominating the development of a technology that is set to be integrated into private and public services globally. Past platform shifts have taught us that authorities must not wait until a market has fully consolidated to intervene.

Competition authorities need to act swiftly and look along the genAI value chain, from chips to platforms, with the specific aim of restricting the ability of tech giants to shape and dominate the development of the technology. Specifically:

- Cloud services must be investigated, and dominance must be structurally limited either by imposing utility-style regulations or structurally separating the companies.

- Partnerships with, and investments in, smaller companies must be investigated not just as isolated events but as components of potential anti-competitive strategies.

- Dominant players should be forced to implement interoperability standards and enable easy switching between clouds.

Support our work

Would you like to support investigative research that challenges unjust corporate power? We do action-oriented research to expose corporate harm, debunk myths, and unlock new alternatives.

Your contribution helps us stay independent, factual, and bold.

Do you need more information?

-

Margarida Silva

Senior Tech Researcher

Related news

-

-

EU sides with Big Tech as Google’s Wiz takeover gets a green lightPosted in category:Published on:Statement

-