Greenlighting Abuse

Audits and certifications failed to identify sexual harassment and abuse at Kasigau

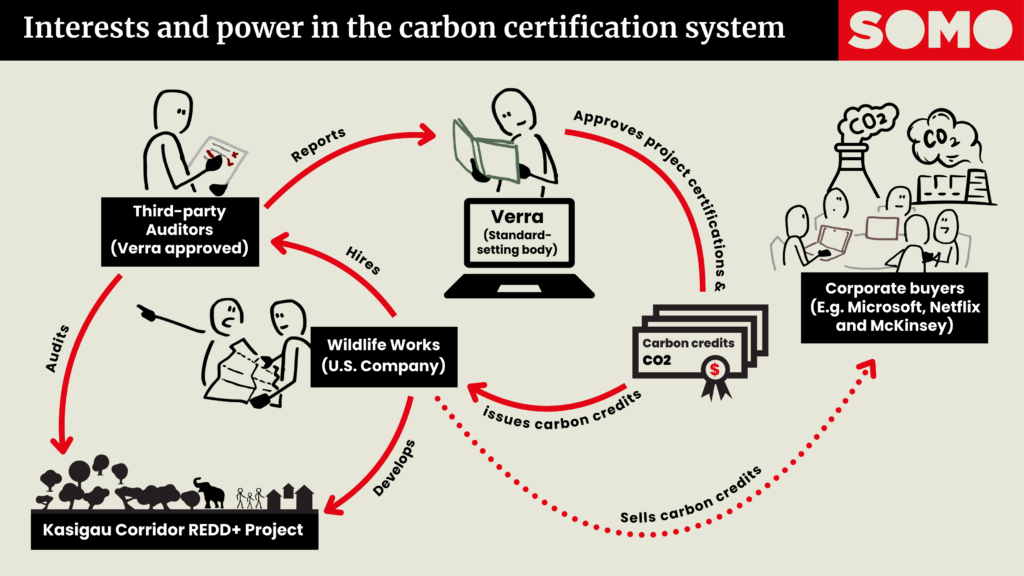

The Kasigau Corridor Project in Kenya is a high-profile carbon offsetting project that claims to ‘avoid’ emissions by protecting forests. When ‘Ernst Wood’ (a pseudonym)1 arrived at Kasigau, his task was clear: to evaluate whether the project, which is run by US-based company Wildlife Works Carbon (Wildlife Works), met the environmental and social criteria needed to maintain its ethical certifications.

Social and environmental auditors such as Ernst are rarely mentioned in the debate around forest-based offsetting schemes, yet the carbon credit market could not exist without them. That’s because many buyers of such carbon credits – often big polluters, such as fossil fuel companies and airlines – rely on ethical certifications as evidence that the offsetting projects on which these credits are based have real social and environmental benefits. Certificates give credibility to the impact claims that businesses such as Wildlife Works make about their forest protection or tree planting projects and can boost the green credentials of their customers.

At the time of Ernst’s visit, Wildlife Works boasted not one but two certificates: the Verified Carbon Standard (VCS) and the Climate, Community and Biodiversity Standards (CCB), both issued and supervised by the Washington-DC-based organisation Verra. The VCS is, in theory, supposed to confirm whether offset schemes plant or save as many trees as they purport to do. The main promise of the more expansive and community-focused CCB is that offsetting projects carrying its label deliver positive socioeconomic outcomes, such as income generation opportunities for local people and greater gender equality.

Audits are the main tool used by carbon certification schemes like Verra to monitor the environmental, social, and human rights impacts of offsetting projects. Wildlife Works has long held up its CCB label as proof that its operations at Kasigau go well beyond basic social safeguards by ‘empowering’ the local community – especially women – through jobs and various development initiatives, known as ‘co-benefits’. Many of its customers have repeated this claim, with Netflix going so far as to make and promote a short film about the Kasigau project(opens in new window) . By emphasising how Wildlife Works supports women’s groups and employs female rangers – an occupation traditionally reserved for men – the film depicts Kasigau as an essentially feminist project that’s entirely beneficial for local people.

Even international development organisations, such as the United Nations Environmental Programme (UNEP), have held up(opens in new window) Kasigau as a model of how to wed climate goals with community benefits.2

The foundation for this glowing image comprises over a decade of auditing reports put together by individual auditors such as Ernst and the auditing companies for whom they work, which ‘verify’ the environmental and social impact claims made by Wildlife Works. Yet, as Ernst’s experience at Kasigau shows, the fact that auditors sign off on projects does not mean they have found no problems. In fact, Ernst’s visit to Kasigau caused him serious concerns that for many Wildlife Works employees there, especially women, the daily reality was far from empowering or even safe.

Ernst heard stories of how senior men in the company had tried to coerce junior female colleagues into having sex with them. He found these allegations “very upsetting” but could not write them down in his report because “no one wanted to go on the record”.3 Employees were prepared to share their stories only “in confidence”.

With people too scared to have their stories as part of the official audit record, Ernst saw no other option than to finalise his report without referring to such issues. But he left Kasigau feeling deeply unsettled, suspecting something was seriously wrong at the project.

In 2023, an investigation into Kasigau by the Kenya Human Rights Commission (KHRC) and the Centre for Research on Multinational Corporations (SOMO) showed that Ernst’s concerns were well founded. Drawing on interviews with over 30 employees and community members, both victims and witnesses, KHRC and SOMO documented multiple allegations of predatory men within Wildlife Works who had exploited positions of power to sexually assault, harass, and extort sex from female staff and mistreat vulnerable women in the wider community. According to multiple sources, the abuses had been going on for a decade.

These revelations from KHRC and SOMO prompted Wildlife Works to commission a law firm to carry out an internal investigation. This led to the(opens in new window) dismissal of one individual “for gross misconduct, including conduct in violation of the company’s policy against sexual harassment”.4 Wildlife Works also terminated(opens in new window) the employment of its local HR manager because he had “created a culture of fear and intimidation that, according to interviewed personnel, prevented reporting of sexual harassment incidents”.

A decade of auditing failures

Ernst was not the only auditor to review Kasigau while egregious abuses were taking place. Between 2013 and 2022, four US-based auditing firms sent teams to the project site, with each of them reportedly interviewing dozens of employees and community members on topics such as working conditions, rights, and community impacts (see table). None of them reported finding any evidence of sexual harassment or abuse.

| Company | Location | Year audit release | Type of verification |

| Environmental Services, Inc. | USA | 2013 | CCB v2 |

| SCS Global Services | USA | 2015; 2018 | CCB v2 VCS v3, CCB v2 |

| S and A Carbon | USA | 2020; 2022 | CCB v2, VCS v4 CCB v2, VCS v4 |

| Aster Global Environmental Solutions | USA | 2021 | CCB v2, VCS v4 |

Yet, as community members told KHRC and SOMO, it was an open secret among employees and the wider community that, in the words of one interviewee, women were “treated as sex objects” at Wildlife Works, and that the perpetrators got away with it by “intimidat[ing] everybody”.

Instead, the auditors’ findings were reassuring and flattering towards Wildlife Works’ culture and project management. They found that the project had “overwhelmingly … positive impacts to the local communities”,5 was “highly unlikely to result in any net negative impacts on local stakeholders”,6 and was committed to “equal opportunity employment”.7 “In conversations with staff,” one audit report noted, “it was learned that no negative comments or grievances were ever received.”8

The collective failure of these auditors is shocking but not surprising. This is because the auditing system – a largely unregulated web of private companies that compete for contracts from offset project developers – is set up in such a way that it’s nearly impossible for auditors to meaningfully investigate and report on abuses. What emerges as a result is a ‘paper reality’ that is at best incomplete and, at worst, a fiction, replete with misleading reassurances around the wellbeing of some of the world’s most marginalised communities.

The reasons the auditing system failed so spectacularly at Kasigau appear inherent in the system. These include the power imbalance between local people (both employees and other members of communities) and carbon project developers; the limitations placed on auditors, restricting the scope of their reviews; the auditors’ bias in favour of the project developers who are their clients; and the conflict of interest in the relationship between auditors and project developers. We consider each of these reasons in turn below.

SOMO wrote to the auditing companies listed in the table above. Only SCS Global responded, telling us that its assessment team had not heard or received any “allegations about sexual harassment or assault”.9

The power imbalance

Ernst’s suspicion that things were not as they seemed was triggered by his discussions and informal chats with Wildlife Works’ local staff. During these conversations, Ernst heard disturbing stories of what women at the company were put through by more senior male colleagues. For example, he learned about an incident where a female employee asked for an advance on her salary and was told that “she had to ‘earn it’ by providing sexual favours”. In another incident, a woman had allegedly been “pressured repeatedly to sleep with a more senior colleague”.

Ernst said he had tried, but failed, to get interviewees to speak about these and other problems on the record, but that staff members

“and especially junior staff, seemed unable to speak freely. I had the impression that they had been told what to tell us and were afraid to defy these instructions. While I tried to convince them that they could share problems with me, I left those interviews feeling they were afraid to open up.”

Project employees were not the only group Ernst believed to be holding back during interviews. Community members, he explained, “who benefit from project carbon revenues are less likely to share [problems], as doing so may risk the continuation of project benefits”.

As a result of these power asymmetries and the apparent lack of trust in the audit process on the part of Ernst’s interviewees, none of his concerns made it into his audit report.

The barriers Ernst ran into during his audit shine a light on how the power imbalance between offset project developers, on the one hand, and their staff and local communities, on the other, shapes audit outcomes. In theory, the interviews used to monitor the social impacts of an offsetting project are more straightforward than the messy and discredited(opens in new window) methods used to calculate carbon emission reductions. However, in practice, local employees and communities have good reasons to keep their concerns to themselves.

Staff might, for example, have been told by their boss what to tell (or not tell) the auditors, as Ernst suspected had happened at Kasigau. In other cases, auditors might conduct interviews accompanied by a manager from the project developer. Ernst, based on his experiences, believes this to be “common practice” despite the obvious limiting effect that such managerial presence can have on the ability of staff to speak openly about problems.

Limitations placed on auditors

Social and environmental audits are, at best, a snapshot in time based on a small sample of source interviews and, generally, a review of documents. Auditors appear at a project every few years for just a few days. They would need to “speak to hundreds of people” to make sense of the social impacts of an offsetting project, according to Ernst, whereas in reality “it’s more likely [they will only speak with] dozens”. The truth, Ernst told us, is that “it’s very limited what we can find out in such a short period of time”.

As Ernst also noted, audits can be manipulated, particularly if the verification system limits the scope of inquiry. SCS Global appears to agree, telling SOMO: “[A]dequate consultation with communities may require numerous engagements over a lengthier period of time than has sometimes been afforded to the validation and verification body. Indeed, some of our requests for added time are met with great resistance.”

The power asymmetries between companies like Wildlife Works and communities, combined with the limitations the system places on auditors, fundamentally disadvantage workers and communities. Companies have a responsibility and, increasingly, a legal obligation, to account for and report on the impact of their activities on people and the environment. While some see social and environmental audits as a tool to deliver on this responsibility, the flaws of such processes have been repeatedly exposed(opens in new window) by civil society organisations.

Bias in favour of clients

In 2020, one or more community members living around Kasigau chose to remain anonymous when they tried to report concerns to S&A Carbon, which audited Kasigau that year. These concerns related to the allegedly “unfair hiring practices” of Wildlife Works’ Human Resources Department. According to S&A’s audit report, the written complaint called for the “removal” of Wildlife Works’ HR Manager at Kasigau and for people “to be treated with respect and dignity”.10 Although the audit report is vague on the exact content of the complaint, it suggests it also raised unfair termination practices as an issue.11

In their report, S&A’s auditors claimed they were unable to do any meaningful follow-up because the field visit was completed at the time they received the complaint and the coronavirus pandemic restricted their movement. They also argued that the anonymous nature of the grievance prevented them from speaking to the complainant – a position that wrongly implies that speaking to a complainant is necessary to investigate allegations.

More concerningly, S&A accepted, seemingly without any attempt at verification, Wildlife Works’ assertion that the complaint was “based in personal conflict between the individual(s) and the project and that therefore the discrimination accusations have no merit”.12 The auditors reported that Wildlife Works “believes they know the identity or at least the family who raised the comment” and “is confident that the letter originated from [location redacted by SOMO]”.13 To respond to the issue, the auditors go on to explain, Wildlife Works planned to hold community meetings in the location it assumed the grievance stemmed from. 14

One obvious problem with S&A’s handling of this complaint is how its apparent bias towards Wildlife Works’ version of events led it to largely disregard the concerns of one or more community members. Equally troubling is how S&A chose to include in its public report a presumed characteristic of the anonymous complainant(s) – the name of their location – that could very well lead to identification. It is not difficult to see how S&A’s handling of this complaint could have a chilling effect on employees or other members of the community, who might think twice before reporting concerns.

One year later, Aster Global visited Kasigau for Wildlife Works’ 2021 audit. The auditors, who were aware of the anonymous complaint filed the previous year, should have had additional cause for concern around Wildlife Works’ hiring and termination practices. Three similar complaints had been made through Wildlife Works’ grievance system.15 Despite this additional evidence of problems related to human resources practices, Aster Global’s audit report does not mention the new complaints, and there is no evidence that the auditors investigated the issues. 16

The apparent failure to investigate such signals about potential problems more deeply may help explain why a decade of auditing failed to uncover any of the abuses that KHRC and SOMO have exposed.

This seeming tendency of auditors to give clients the benefit of the doubt is no anomaly in the carbon-offsetting world. Recent research(opens in new window) by the Goldman School of Public Policy, University of California, Berkeley, has shown such auditors’ bias to be pervasive in the industry. The Berkeley researchers reviewed project descriptions and audit reports on Kasigau and 17 other forest-based offsetting projects. They found that safeguarding compliance appears to be “systematically rubber-stamped despite evidence of noncompliance”.17

“Time and again,” the Berkeley researchers explain, “projects received positive verifications despite woefully inadequate consultation, evidence of contested land claims, and even violent evictions.” Auditors accept problematic community engagement practices and consistently give their clients “the benefit of the doubt”, “while doing minimal due diligence” on their claims.

Conflict of interest

The commercial relationships between auditors and the developers that run carbon offsetting projects have a profound impact on how auditors engage with employees and communities and interpret the testimonies given to them. Like offsetting, more broadly, auditing is a profit-driven industry where firms compete for contracts from companies such as Wildlife Works. Auditors receive payment for their services from the very same company whose behaviour and impacts they are supposed to scrutinise.

As an auditor, asking tough questions on community relations, and digging deeper than your rivals on issues like working conditions, is therefore unlikely to make you popular with a clientele whose ability to sell credits hinges on having positive outcomes highlighted by their audit reports. This creates an inherent conflict of interest at the heart of the audit system, which can undermine the confidence that local staff and community members have in the auditors in whom they are expected to confide.

This does not mean that auditors deliberately ignore problems, but it presents them with an incentive to give clients the benefit of the doubt. As Ernst explained, the market reality imposes pressure on auditors that “limit the level of investigation” they can apply.

Conclusion

Sexual harassment and abuse and a culture of fear created by a HR manager were a reality at Kasigau. Audit firms repeatedly failed to identify or report on this reality. These firms operate within a system and to a standard that made it seem impossible for at least one auditor to raise their serious concerns about women’s safety at Kasigau.

Ernst Wood spoke to KHRC and SOMO because he worries that the people who end up paying the price for the structural shortcomings of the auditing system are those who are often already marginalised. He wants to see the damage done by the system repaired.

Individuals like Ernst play a critical role in bringing the truth to light, but it is not easy for them to do so. This is because both the carbon offsetting industry and the carbon certification industry are exactly that: industries, governed by competitive pressures, profit objectives, and private interests.

An irreconcilable and dangerous tension exists between such business pressures, on the one hand, and the rights of communities and workers on the other. And this means that even auditors such as Ernst, who are willing to ask tough questions, lack the tools and means to protect and support communities.

Research note

SOMO contacted Aster Global Solutions, SCS Global and S&A Carbon for comments on the sexual harassment and abuse at Kasigau and their failure to identify it. Only SCS Global responded.

SCS Global said:

We stand behind the audit procedures implemented during this assessment. SCS GHG audits are conducted following standard auditing operating procedures in accordance with the rules and requirements of our International Standards Organization (ISO) accreditation under the ANSI National Accreditation Board (ANAB). Above all, SCS employed the standard of care of Validation and Verification Bodies (VVBs) at the time.

As a benefit corporation, SCS is fully committed to driving positive change toward greater governmental and corporate environmental and ethical responsibility. We share your interest in preventing human rights abuses around the world.

In August 2023, SOMO raised the issue of deliberate action to mislead validation and verification bodies in a letter to Wildlife Works. We informed the company:

SOMO received testimony that, prior to auditors coming to inspect the project, Wildlife Works had instructed or coached staff on how to behave and respond. This coaching appeared to be intended to provide a partial, and therefore misleading, picture of the work conditions to the social auditors.

Wildlife Works did not respond to us on this issue.

Endnotes

1 We refer to this person as ‘Ernst Wood’ to protect their anonymity.

2 Since the Kenya Human Rights Commission (KHRC) and the Centre for Research on Multinational Corporations (SOMO) released their report on Kasigau (Offsetting Human Rights, 2023, www.somo.nl/offsetting-human-rights), UNEP has added a disclaimer to its article on Kasigau, stating that it doesn’t officially endorse individual projects; yet the article continues to uncritically repeat Wildlife Works’ claims about Kasigau’s impacts.

3 SOMO interviewed Ernst between 10 and 20 March 2024 by phone. This article includes quotes from these conversations, as well as quotes from interviews done with Ernst in 2023 for the KHRC and SOMO report, Offsetting Human Rights.

4 Wildlife Works Statement, Updates from the Kasigau Project, November 20, 2023, https://www.wildlifeworks.com/post/update-on-kasigau(opens in new window)

5 S&A Carbon, Verification report for the Kasigau Corridor REDD+ project phase II – the community ranches, 2020, p. 54 https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=47114&IDKEY=kkjalskjf098234kj28098sfkjlf098098kl32lasjdflkj909j64970206(opens in new window)

6 Environmental Services Inc, Climate, Community, and Biodiversity Alliance Project Annual Verification Report, 2013, p. 33 https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=41997&IDKEY=j0e98hfalksuf098fnsdalfkjfoijmn4309JLKJFjlaksjfla9857913863(opens in new window)

7 SCS Global Services, Final CCBA Project Verification Report, 2015, p. 24, https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=42218&IDKEY=9kjalskjf098234kj28098sfkjlf098098kl32lasjdflkj909958218622(opens in new window)

8 Environmental Services Inc, Climate, Community, and Biodiversity Alliance Project Annual Verification Report, 2013, p. 18 https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=41997&IDKEY=j0e98hfalksuf098fnsdalfkjfoijmn4309JLKJFjlaksjfla9857913863(opens in new window)

9 See ‘Research note’ above.

10 S&A Carbon, Verification report for the Kasigau Corridor REDD+ project phase II – the community ranches, 2020, p. 16, 81-85 https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=47114&IDKEY=kkjalskjf098234kj28098sfkjlf098098kl32lasjdflkj909j64970206(opens in new window)

11 S&A Carbon, Verification report for the Kasigau Corridor REDD+ project phase II – the community ranches, 2020, p. 83-85 https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=47114&IDKEY=kkjalskjf098234kj28098sfkjlf098098kl32lasjdflkj909j64970206(opens in new window)

12 S&A Carbon, Verification report for the Kasigau Corridor REDD+ project phase II – the community ranches, 2020, p.82 https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=47114&IDKEY=kkjalskjf098234kj28098sfkjlf098098kl32lasjdflkj909j64970206(opens in new window)

13 S&A Carbon, Verification report for the Kasigau Corridor REDD+ project phase II – the community ranches, 2020, p.82-83 https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=47114&IDKEY=kkjalskjf098234kj28098sfkjlf098098kl32lasjdflkj909j64970206(opens in new window)

14 S&A Carbon, Verification report for the Kasigau Corridor REDD+ project phase II – the community ranches, 2020, p.83 https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=47114&IDKEY=kkjalskjf098234kj28098sfkjlf098098kl32lasjdflkj909j64970206(opens in new window)

15 This audit required the Aster Global auditors to review the anonymous complaint raised earlier. See Aster Global Environmental Solutions, The Kasigau Corridor REDD+ Project Phase II – The Community Ranches, 2021, p. 51-52, https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=59529&IDKEY=f0e98hfalksuf098fnsdalfkjfoijmn4309JLKJFjlaksjfla9k82090491(opens in new window) . A 2021 accuracy review(opens in new window) by Verra of an audit by Aster Global Environmental Services of the Kasigau Corridor REDD+ project Phase II reveals (p.4) that of all concerns filed through the Wildlife Works grievance system in the previous year, three “were identified as rising to the level of potential dispute between the project and communities or other stakeholders, with these three involving concern over hiring or termination practices”. According to Verra’s report, which was still ‘pending’ at the time of writing, “[t]he short-term resolution identified for these [concerns] was for the community relation and HR department to organize HR employment and working procedures in the complainant’s’ [sic]communities after the Covid pandemic abates”. Aster Global’s audit report does not give any details around the nature of the concerns raised through Wildlife Works’ grievance system. Aster Global Environmental Solutions, The Kasigau Corridor REDD+ Project Phase II – The Community Ranches, 2021, p. 17, https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=59529&IDKEY=f0e98hfalksuf098fnsdalfkjfoijmn4309JLKJFjlaksjfla9k82090491(opens in new window)

16 Aster Global Environmental Solutions, The Kasigau Corridor REDD+ Project Phase II – The Community Ranches, 2021, p. 17. https://registry.verra.org/mymodule/ProjectDoc/Project_ViewFile.asp?FileID=59528&IDKEY=f097809fdslkjf09rndasfufd098asodfjlkduf09nm23mrn87m82089112(opens in new window)

17 ‘Quality Assessment of REDD+ Carbon Credit Projects’ (2023) by Berkeley Carbon Trading Project (2023), p. 177- 179.

Do you need more information?

-

Maria Hengeveld

Corporate Researcher

Related news

-

Responses to the allegations of sexual abuse at the Kasigau carbon offset project run by Wildlife WorksPosted in category:Published on:Statement

-

Systemic sexual abuse at celebrated carbon offset project in KenyaPosted in category:News

Systemic sexual abuse at celebrated carbon offset project in KenyaPosted in category:News Maria HengeveldPublished on:

Maria HengeveldPublished on: -